This article covers:

The old Arnott’s catchphrase dates back a century: “There’s no substitute for quality.” It’s simple, and it captures the heart of how resilient businesses, and resilient portfolios, are built.

It also happens to be an ideal way to think about markets today, particularly credit markets. The lens to look at everything through is Quality. Because there is no substitute.

Over several decades, credit has attracted strong interest. Investors have been drawn to a combination of steady income, attractive headline returns, and a long period of low losses. But ‘credit’ is a label that encompasses a vast array of products and an even broader universe of underlying assets. This can include diversified mortgage portfolios, unsecured corporate loans, even complex products like bundles of ‘collateralised loan obligations.’

But how to find quality? In calm conditions, all these investments can look reassuringly stable. Everything looks orderly when nothing is under strain. But history has shown how calm conditions don’t last forever. That’s where the importance of quality kicks in.

Periods of market stress are the quality audit for which no one asks and for which few prepare.

Don’t panic.

Markets are never far from volatility, and right now we’re seeing headlines of economic and geopolitical forces creating stress in some sectors.

At La Trobe Financial, we’ve been managing credit portfolios since 1952. We’ve seen a thing or two, and we’ve seen credit cycles ebb, flow, and shock. One of the lessons of every cycle is that credit stress rarely walks through the front door with a name badge on. And it hits the lower-quality strategies first:

- economic activity cools

- higher interest costs bite

- refinancing becomes harder

- cash buffers grow ever thin

- strategies built on weaker fundamentals start to fail

Bad loans are written in good times, as the saying goes. Or the structure that sounded good on paper, suddenly can’t meet the requirements of a market stress event.

It’s no surprise, then, that investors are shifting their attention away from chasing the highest yield and back to valuing the peace of mind that quality brings.

Know your product

As we said, credit is an enormous global market, and the label captures enormous variation of assets and enormous variation of managers. Some providers have decades of experience and have navigated genuine periods of stress. Others have emerged more recently and have yet to be tested across the credit cycle.

If stress does start emerging in credit markets it will highlight that:

- underwriting standards differ

- risk models differ

- valuation practices differ

- loan‑to‑value ratios, covenants, sector exposures, borrower selection — no two approaches are alike

- liquidity management differ

The lessons of history are clear. Real quality matters. Expect divergence between manager outcomes in the period ahead as investors rediscover quality.

It’s audit time

Not all providers will pass. As the cycle turns and outcomes diverge, managers with well‑structured portfolios, conservative assumptions and strong security positions will have the resilience they need. Others not so.

Now is the right time to be asking the hard “what if” questions of your fund manager. Because some will be found out for having taken easy choices during good times, which will now be working against them. Or those who took chances with complex structures, riskier assets, or less diversified portfolios. Some providers will be exposed while others will shine.

As conditions tighten, questions become sharper:

- How conservative were the original loan structures?

- How realistic were the valuations?

- What assumptions were made about borrower resilience?

- What margin for error was built in?

- Is the portfolio truly diversified?

- What is the real liquidity position of a portfolio?

The answers to all of these questions are based on decisions often made years earlier. It’s too late to fix loan structures once a borrower is already under pressure. Or quickly build buffers when capital is at risk. Or shuffle the deck chairs to eke out some liquidity when investors start to panic.

Our approach, and why it matters

At La Trobe Financial, quality runs core to our convictions. Across both our Australian and U.S strategies we embed quality across our asset origination, underwriting, valuation discipline, liquidity, and wider portfolio management. We do that because our 130,000 investors^ have trusted us with their hard-earned savings to live throughout their prosperous retirement. So rather than crossing our fingers and hoping for the best, we build our portfolios to perform at all points along the economic cycle.

Each of our portfolio accounts are distinct offerings. Each is designed with distinct outcomes in mind, to suit a range of investor needs. But one thing is certain: Each represents our view on the best way to deliver stability and performance based on the assets it can invest in, and the duration investors can invest for.

It’s all about quality assets, held within quality structures, managed by quality people.

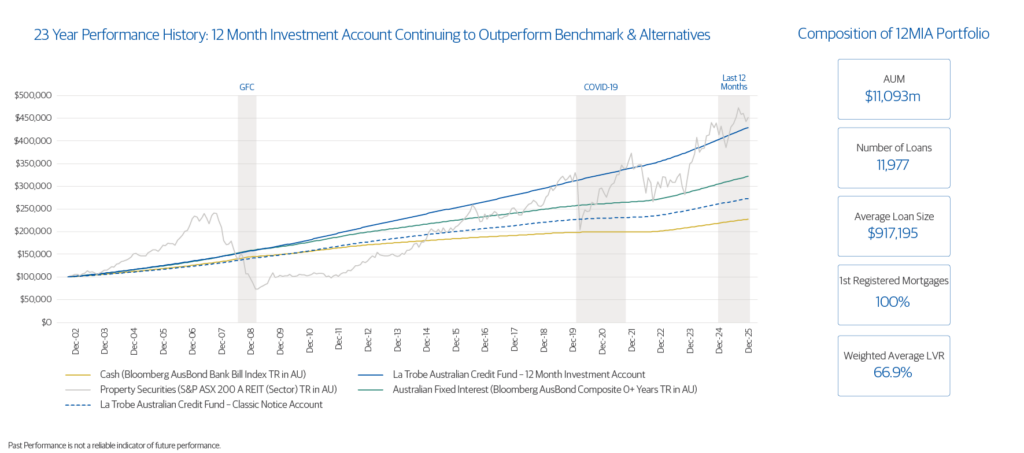

La Trobe Australian Credit Fund

The $14bn La Trobe Australian Credit Fund exemplifies these characteristics. For longevity, diversification and track record – the ultimate proof of quality – it is entirely unlike any other offering in market. It has 14,203 high-quality loans, all secured by registered first mortgages over property here in Australia. The average loan to value ratio of its loans is just 67.4%. And our unique liquidity management framework has delivered flawless liquidity to investors for decades, including during the Global Financial Crisis and the COVID-19 pandemic.

Our flagship Australian strategy is the best in class 12 Month Investment Account. This is a highly diversified portfolio delivering investors a variable monthly income and stable capital with zero investor losses in its 23-year history.

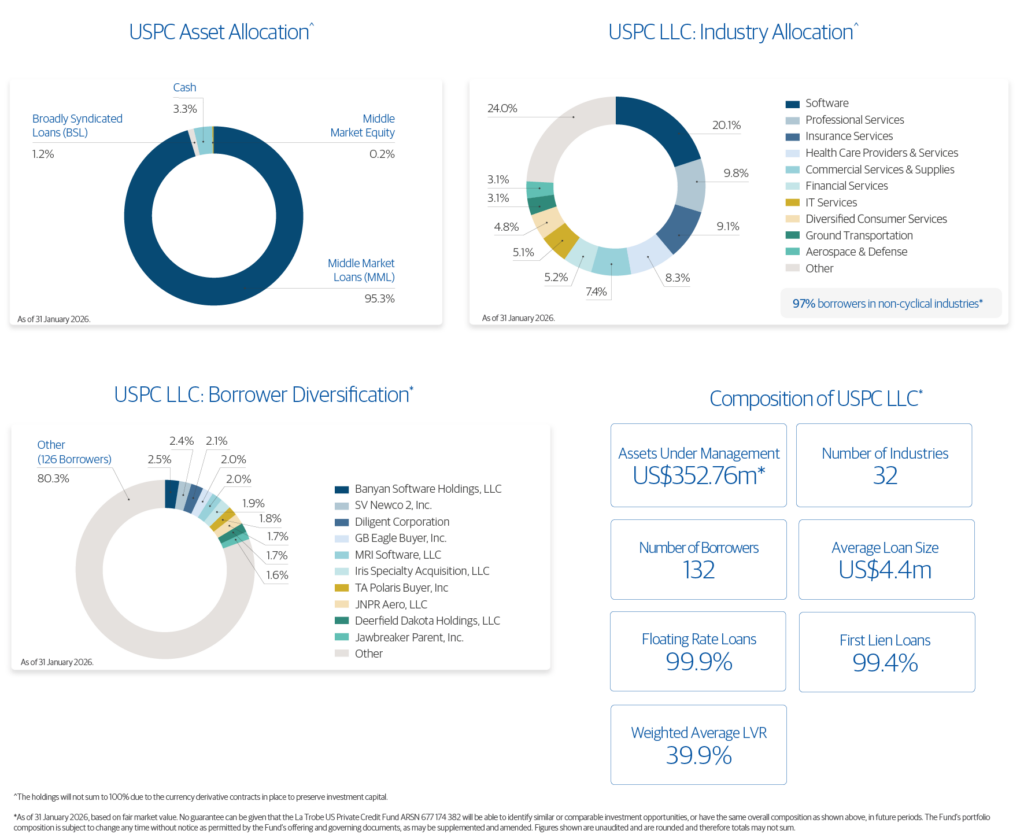

La Trobe US Private Credit Fund

Launched in 2023, our U.S strategy provides more opportunity for variable return, diversified credit investment. And the same principles apply with quality assets, in a quality structure, prepared by a quality manager.

The La Trobe US Private Credit Fund is pure-play exposure, at work in America’s engine room, the U.S middle market. A carefully constructed, diversified portfolio of first‑lien, low LVR loans, highly diversified by borrower and sector. And the stats, which we make available on our website each month back this up.

The portfolio comprises low Payment In Kind (PIK) loan numbers, loans performing per their documented terms, and minimal non-accruals. This is a quality portfolio, within a quality structure. Underlying assets are originated via our product partner, Morgan Stanley, and their North American Private Credit Team. These are quality, conservative, and experienced managers delivering on a mandate for low volatility returns for investors.

No substitute

One thing is certain. Market volatility will continue. And investment strategies built on poor foundations will suffer.

But don’t panic. It’s simply time to pay attention.

Understand the dispersion within credit. Not all managers are investing in the same quality assets with the same discipline. Understand the structure, and each manager’s true ability to generate liquidity so you can access your money when you need it. Understand the manager, and their demonstrated ability to manage their assets across moments like this.

In the long term, the best results are always delivered by quality assets, held within quality structures, managed by quality people. And there’s no substitute for that.

^ Total investors is calculated by adding all individual & joint investors (which includes some investors with a current zero balance in their account) to reasonable estimates of investors investing via trusts or SMSFs.

La Trobe Financial Asset Management Limited ACN 007 332 363 Australian Financial Services Licence No. 222213 is the responsible entity of the La Trobe Australian Credit Fund ARSN 088 178 321 and the La Trobe US Private Credit Fund ARSN 677 174 382. It is important that you consider the relevant Product Disclosure Statement (PDS) before deciding whether to invest or continue to invest in the fund. The PDSs and Target Market Determinations are available on our website.

Any financial product advice is general only and has been prepared without considering your objectives, financial situation or needs. You should, before investing or continuing to invest in the La Trobe Australian Credit Fund & La Trobe US Private Credit Fund, consider the appropriateness of the advice having regard to your objectives, financial situation or needs and obtain and consider the relevant Product Disclosure Statement for the fund.

Past Performance is not a reliable indicator of future performance.